When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

Even if I had millions in the bank, the businessman/investor in me would always think about how to better use this money to augment it further.

I know a fair number of really wealthy people. I don't know anybody who doesn't have full coverage on their vehicles. It's really inexpensive and it's one of the only things good about socializing anything!

Any fool can make money...it's the smart people who keep it.

I know a fair number of really wealthy people. I don't know anybody who doesn't have full coverage on their vehicles. It's really inexpensive and it's one of the only things good about socializing anything!

Any fool can make money...it's the smart people who keep it.

Umm, well, I certainly would not call it "inexpensive" to insure a modern F-type, but relative to what could happen if you do not have it in place, well yeah....Looking super cheap ;-)

I say this as someone who just put insurance on a 2024 R yesterday here in Canada. I've talked about this in another thread somewhere, but these F-types have become shockingly expensive to insure in a very short time period in relative terms (at least in my market). I could insure a 911 for half of what I'm paying on this F-type. I got a quote 4 months ago and the price to insure at that time was going to be similar to the 911. Not anymore. My insurance guy is supposed to be getting an "actuarial report" to explain why. Doesn't really matter, because I need to pay it, but I definitely am curious what inputs lead to that happening basically overnight. Very weird to me, but I think lots of things are changing in the insurance industry these days with high levels of theft (It's out of control in central Canada where I live), EVs that are guaranteed write offs if they drive over a pebble, etc...

I searched high and low for a better rate than my current insurer that I've been with for over 25 years and I could not find one. I'm 49, no accidents or speeding tickets, have all my insurance with them (Home, 2 other vehicles, life insurance, some other products, etc)...

I will look at Hagerty 3 years from now when I'm eligible to see if I can do better, but it looks like that will be my only opportunity for a better rate. I tried to get a quote from them but they said I need to have been "driving a car like that for at least 3 years" before they would even consider me (at least in Ontario, Canada). Seems a bit ridiculous to me, but that was one of their criteria.

Another thing that can make a huge difference for people is the fact that in Canada you pay full rate for each car you own. In the US, at least in some regions, they don't charge you full rate on each car. This makes more sense to me, it's not like I can be concurrently driving all 3 of my vehicles at the same time ;-)

In any case, I think most people don't like feeling like they are overpaying on auto insurance. Is what it is I guess.

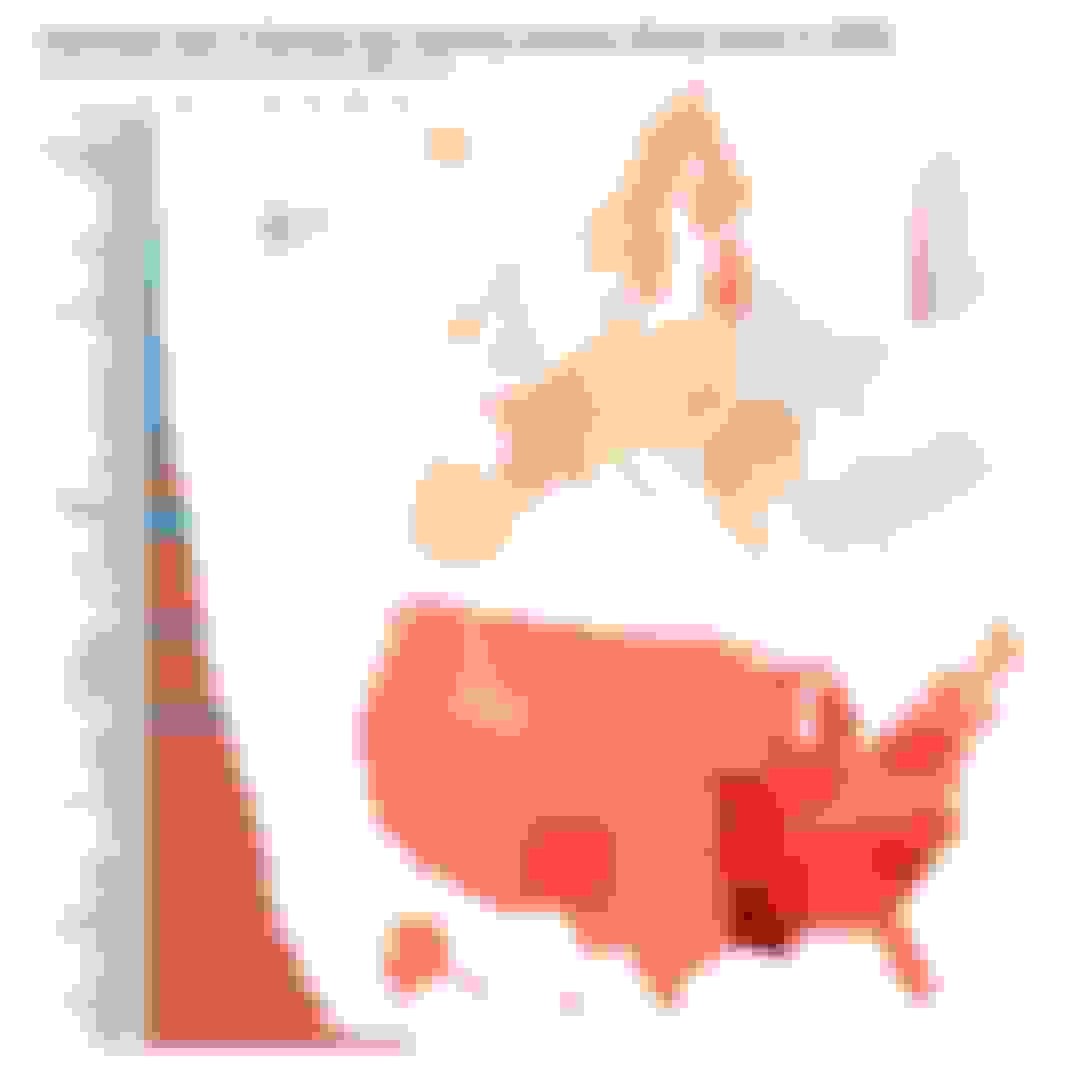

That might come as a surprise to some but no, I didn't realize this problem is so huge in the US. Reading this topic I was dumbfounded why everyone seems to be focusing on uninsured drivers while I was mostly aiming my question on the odds of causing the collision without having the comprehensive insurance and having to repair your own car out of your own pocket. This danger of uninsured drivers causing a collision didn't even cross my mind as official statistics say that 99 % drivers in Europe (where I come from) are insured. Some countries like Germany and Finland have no uninsured drivers at all. Literally 0.0 %. While in the US the percentage of uninsured drivers is a whooping 14%, in Florida even 25%.

Knowing this now, I should've posed my question something like "If there were no uninsured drivers on the roads, would you still pay the full comprehensive insurance for $2000 or just the mandatory insurance for $300?"

I personally find that hard to believe. There are irresponsible people in all countries. When humans are involved this is pretty much guaranteed. There is no way this is only a North America thing. Not sure where you are getting your info. Feel free to post up a link, I'd be curious.

That is almost tantamount to saying that there are no murders in your country as far as I'm concerned. It is required that all people on the road have insurance over here. They just choose to break the law. Pick any topic and law breakers will exist in my view.

Since we've found out that we have nothing in common in Europe and US regarding the mandatory insurance, this topic can be locked/removed. It serves no purpose unless I open a new topic and pose the question differently. I live in Europe where 99 % of cars are insured for 3rd party liability up to 1 million euros by law. So, I'm not motivated to pay $2000 each year just because I might crash my sparsely driven weekend car through my own fault.

If we can recommence the conversation with this new outlook, the topic can still be useful otherwise please close it. I thank everyone for their valuable opinions and experiences. Have a good weekend.

You opened the topic. People are responding. The law of averages can find anyone. That is the true reality man. To think otherwise, quite frankly, is naive. I'm sincerely not intending to offend here at all.

You should do what works best for your head at the end of the day obviously. You asked some strangers on the Internet for input and it was given.

In any case, I think most people don't like feeling like they are overpaying on auto insurance. Is what it is I guess.

I believe that most people believe they are over-paying for ALMOST EVERYTHING...and they are 100% correct! In a financial/political/social system that has been incredibly corrupted by all kinds of nefarious players, we are all paying for the theft. Just look at what inflation has done to the average person over the last few years. But that's a different matter.

Even with all the fraud going on, most forms of insurance are still worthwhile [especially if you can partially self-insure where prudent].

I believe that most people believe they are over-paying for ALMOST EVERYTHING...and they are 100% correct! In a financial/political/social system that has been incredibly corrupted by all kinds of nefarious players, we are all paying for the theft. Just look at what inflation has done to the average person over the last few years. But that's a different matter.

Even with all the fraud going on, most forms of insurance are still worthwhile [especially if you can partially self-insure where prudent].

Very true these day...lol...The inflationary environment we are in has definitely messed with peoples' heads for sure. No doubt ;-)

I personally find that hard to believe. There are irresponsible people in all countries. When humans are involved this is pretty much guaranteed. There is no way this is only a North America thing. Not sure where you are getting your info. Feel free to post up a link, I'd be curious.

I even found out today that if you're hit by an uninsured driver in the EU, the government pays for damages to property and persons up to 1.2 million and 6 million respectively. So you don't have to worry even about that one percent.

I live in Central Europe (the green part) where the percentage is virtually zero.

I even found out today that if you're hit by an uninsured driver in the EU, the government pays for damages to property and persons up to 1.2 million and 6 million respectively. So you don't have to worry even about that one percent.

I live in Central Europe (the green part) where the percentage is virtually zero.

Umm, well, I certainly would not call it "inexpensive" to insure a modern F-type, but relative to what could happen if you do not have it in place, well yeah....Looking super cheap ;-)

I say this as someone who just put insurance on a 2024 R yesterday here in Canada. I've talked about this in another thread somewhere, but these F-types have become shockingly expensive to insure in a very short time period in relative terms (at least in my market). I could insure a 911 for half of what I'm paying on this F-type. I got a quote 4 months ago and the price to insure at that time was going to be similar to the 911. Not anymore. My insurance guy is supposed to be getting an "actuarial report" to explain why. Doesn't really matter, because I need to pay it, but I definitely am curious what inputs lead to that happening basically overnight. Very weird to me, but I think lots of things are changing in the insurance industry these days with high levels of theft (It's out of control in central Canada where I live), EVs that are guaranteed write offs if they drive over a pebble, etc...

I searched high and low for a better rate than my current insurer that I've been with for over 25 years and I could not find one. I'm 49, no accidents or speeding tickets, have all my insurance with them (Home, 2 other vehicles, life insurance, some other products, etc)...

I will look at Hagerty 3 years from now when I'm eligible to see if I can do better, but it looks like that will be my only opportunity for a better rate. I tried to get a quote from them but they said I need to have been "driving a car like that for at least 3 years" before they would even consider me (at least in Ontario, Canada). Seems a bit ridiculous to me, but that was one of their criteria.

Another thing that can make a huge difference for people is the fact that in Canada you pay full rate for each car you own. In the US, at least in some regions, they don't charge you full rate on each car. This makes more sense to me, it's not like I can be concurrently driving all 3 of my vehicles at the same time ;-)

In any case, I think most people don't like feeling like they are overpaying on auto insurance. Is what it is I guess.

Honestly in my experience Hagerty will just make up another requirement when you satisfy that one. Or they will put heavy restrictions on your driving when you do qualify. They told me I wouldn't be able to drive to the grocery store or go shopping. I don't think they're worth using if you can barely even drive the car. I'm under 30 though so I might have crazier restrictions.

Honestly in my experience Hagerty will just make up another requirement when you satisfy that one. Or they will put heavy restrictions on your driving when you do qualify. They told me I wouldn't be able to drive to the grocery store or go shopping. I don't think they're worth using if you can barely even drive the car. I'm under 30 though so I might have crazier restrictions.

Can�t go to the grocery store? Lol

Is this a real example or were you exaggerating a bit to make a point?

Geez, hope yer wrong. Regardless, interesting to hear you say that. Are they not in the business of making money?

Best to read up on the facts, rather than guess, surmise,, or believe misinformation..

It could be your age,, your driving record, or something else that makes them disinclined to insure you. I am female, over 30 and have a stellar driving record. No issues in the past week, adding a 2017 F and 2018 corvette to the Hagerty policy, while saving over $800 annually, having agreed value and no deductibles. Go figure.

Best to read up on the facts, rather than guess, surmise,, or believe misinformation..

It could be your age,, your driving record, or something else that makes them disinclined to insure you. I am female, over 30 and have a stellar driving record. No issues in the past week, adding a 2017 F and 2018 corvette to the Hagerty policy, while saving over $800 annually, having agreed value and no deductibles. Go figure.

Hagerty will obviously have different criteria in different countries/regions.

Up here the first and only criteria I failed to pass was that I had no experience driving �a car like this�. It felt like they were talking to me like I was 16 after hearing that, lol, but thems the rules for them here. Not sure if I would have had any issues after passing that. I doubt it. They politely told me that they would be happy to insure me 3 years out.

Is this a real example or were you exaggerating a bit to make a point?

Geez, hope yer wrong. Regardless, interesting to hear you say that. Are they not in the business of making money?

No they told me that on the phone. When I legitimately laughed he backtracked a bit and said he would need to talk to an adjuster to confirm exactly what I could do but the fact that those type of restrictions seemed to be on the table didn't make me feel confident. It seemed they're primarily for old dudes going to cars and coffee a few times per month and that's about it. I know you 100% can't commute to work or daily drive it. If you don't drive the car what are you even paying them for?

Best to read up on the facts, rather than guess, surmise,, or believe misinformation..

It could be your age,, your driving record, or something else that makes them disinclined to insure you. I am female, over 30 and have a stellar driving record. No issues in the past week, adding a 2017 F and 2018 corvette to the Hagerty policy, while saving over $800 annually, having agreed value and no deductibles. Go figure.

Yeah you've been with hagerty longer than I've been alive so that's probably the biggest factor. The link you sent didn't have any additional info though. I can only say what they told me on the phone and that it seemed like they were treating me like a little kid haha. I also have a great driving record but I drive an SVR and that seemed to scare the **** out of them.

Is this a real example or were you exaggerating a bit to make a point?

Geez, hope yer wrong. Regardless, interesting to hear you say that. Are they not in the business of making money?

They are in the business of making money. That's why they only seem to insure if there is an almost 0% chance of a claim. People with many cars that barely get driven, garage queens, etc. I feel like self insuring makes more sense at that point. Give them a call and ask about driving to different locations and it seems to get murky fast which made me a bit worried about the claims process.

The insurer for our collector cars was challenged by me rwhen they told me "Can't go to a grocery store or shopping mall. Only trips to Club events and to a mechanics"

So I asked, "How about club events (drives) that terminate at a restaurant in a shopping mall?"

Of course, they meant that CONSISTENT everyday use (as in the case of a Daily Driver) is what they discouraged. No driving to work or routine shopping. (Of course, we ALWAYS park at the far end of the lots, with no other cars around...except for the inevitable clapped-out Corolla that parks right next to you!)

Our insurance company also waived any restriction on mileage in writing, after reminding them that the national conventions of owners is usually out-of state. Think JCNA's AGM (Annual General Meeting) which was in North Carolina in 2024, and California in 2023.

The insurer for our collector cars was challenged by me rwhen they told me "Can't go to a grocery store or shopping mall. Only trips to Club events and to a mechanics"

So I asked, "How about club events (drives) that terminate at a restaurant in a shopping mall?"

Of course, they meant that CONSISTENT everyday use (as in the case of a Daily Driver) is what they discouraged. No driving to work or routine shopping. (Of course, we ALWAYS park at the far end of the lots, with no other cars around...except for the inevitable clapped-out Corolla that parks right next to you!)

Our insurance company also waived any restriction on mileage in writing, after reminding them that the national conventions of owners is usually out-of state. Think JCNA's AGM (Annual General Meeting) which was in North Carolina in 2024, and California in 2023.

Yeah and who defines "consistent". They do, when you make a claim. Not even sure what you mean by "routine shopping". It's too murky for me. I don't want to need to think about calling my insurance agent because I want to go to chick-fil-a one weekend.

Yeah and who defines "consistent". They do, when you make a claim. Not even sure what you mean by "routine shopping". It's too murky for me. I don't want to need to think about calling my insurance agent because I want to go to chick-fil-a one weekend.

I didn’t realize they were potentially this sticky. My car will definitely not be a daily, and it certainly will not be a commuting car (I work from home), but I don’t want to be having to think about where I might want to take the car when I do drive it. If that is even close to being a thing then, yeah, I wouldn’t bother. It would probably be best to find a way to love my current higher premiums ;-0

I will assess at the time, but yeah…That would be problematic if true…

Honestly in my experience Hagerty will just make up another requirement when you satisfy that one. Or they will put heavy restrictions on your driving when you do qualify. They told me I wouldn't be able to drive to the grocery store or go shopping. I don't think they're worth using if you can barely even drive the car. I'm under 30 though so I might have crazier restrictions.

I looked into several insurance companies on the it stays garaged and rarely driven, I am fully remote work from home for my company.

Geico had all kind of restrictions, It was supper cheap, but I had to call and register it back into policy to drive it, then back out again, NO WAY..

I had Hagerty on my 2001 WS6 heavy modded car, I was swiped off the interstate in the rain and it was totaled, but due to the high agreed price I had on the car, the shop was able to rebuild her, will all of my after market parts, no issues.

I have an 70K agreed policy on my 2015 F Type and it is cheaper than my wife's 2021 VW Areton per year and I have no deductibles and no restrictions.

Well worth it to me.

03-24-2024, 11:43 AM

03-24-2024, 11:43 AM