When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

While the fire inspector was there, he was asked what he thought would have happened had that fire started unchecked...he said it would definitely been a car-b-cue in that garage.

The car has been out of my possession for a little over a week. Instead of working with/through the other insurance company, I've decided to work through my insurance (for various reasons). Both insurance companies have completed their valuations. However, I have not yet accepted the valuation that my insurance company has provided. Of course, it came back short of what I want (as would be expected). I've provided additional information to the adjuster in an attempt to get them to modify their valuation. If/when I make the decision to accept, after some on-going negotiation, I will then have to wait on the subrogation to see where that lands.

Other than those basics, I have postured myself to have other options if things fail with the insurance companies. We all know these processes can be cumbersome and frustrating. But, I'm gonna keep working toward the best solution for me, and not give in to the "well, that's just how insurance works" BS that keeps getting thrown my way.

Thanks for the update. It sounds like things are progressing as expected. Naturally, they're not going to just give you the full price you paid, but they should come up with an offer that covers something with the minimal age/use of your car. With all that's been going on with new/used prices, it hard to guess exactly where that lands, but good comp's will give you perspective and/or ammunition.

The adjuster is still on the clock, so he'll become increasing "interested" in closing your claim. Since you're going through your own policy, you shouldn't have any delay for subrogation. The 2 companies should work that out on their own. Hopefully you have an alternate vehicle to keep you going in the meantime.

Thanks for the update. It sounds like things are progressing as expected. Naturally, they're not going to just give you the full price you paid, but they should come up with an offer that covers something with the minimal age/use of your car. With all that's been going on with new/used prices, it hard to guess exactly where that lands, but good comp's will give you perspective and/or ammunition.

The adjuster is still on the clock, so he'll become increasing "interested" in closing your claim. Since you're going through your own policy, you shouldn't have any delay for subrogation. The 2 companies should work that out on their own. Hopefully you have an alternate vehicle to keep you going in the meantime.

Best of luck.

Thanks...I'm just trying to keep myself informed, keep options open, and maneuver through this silliness without losing too much of my investment (hoping none at all).

I'm keeping in mind that the entire system is rigged against the consumer. But, who the heck wants to go down without a fight?

I still think that this is different enough from a "normal" auto accident claim that I would eek legal help to claim from the contractor directly.

Let the contactor deal with their insurance and your lawyer. No reason why their incompetence should cost you $20K.

When insuring my e type and f type I had an agreed value stated: e type $100k, f type $50k. The value automatically increases by 2% per year. In the event of a total loss I have options on a new purchase and f types are rare in certain colors and configurations. I hope that never happens. An agreed value prevents disagreements and frustration with market value left to the adjuster.

. Cheers Frank

I still think that this is different enough from a "normal" auto accident claim that I would eek legal help to claim from the contractor directly.

Let the contactor deal with their insurance and your lawyer. No reason why their incompetence should cost you $20K.

Right! Those doors are still open. And, the lawyer is there, I just haven't pulled that trigger on that option yet. That's due to the communication channel to the contractor is open, and he says he's willing to make it right. I don't want to have to pay a lawyer if we can agree to end this without litigation. So, keeping my fingers crossed and options open.

Originally Posted by frank barone

When insuring my e type and f type I had an agreed value stated: e type $100k, f type $50k. The value automatically increases by 2% per year. In the event of a total loss I have options on a new purchase and f types are rare in certain colors and configurations. I hope that never happens. An agreed value prevents disagreements and frustration with market value left to the adjuster.

. Cheers Frank

Very interesting. Thanks for that information. I'll look into that.

I have felt your pain. I would suspect that since the vehicle was properly parked and was not running and/or otherwise in use, that this is a "property damage" claim vs an accident claim. There are different standards (at least in Michigan) for compensation including loss of use (car rental even if you weren't insured for that) and I believe the level of depreciation. However, the adjuster is NOT your friend and neither is your insurance company, but when you subrogate (like you have) they actually have to "work" to get your claim processed. Do not be in a hurry, if you can, to settle. The longer you do not settle, the better they will negotiate. Find comps online yourself of truly comparable f-types and show them. Hemmings and Jaguar dealers in high-end communities like Naples, Florida will have the highest prices, not ebay or shitty 2-star used car dealers in Podunk. (Disclaimer: I truly have nothing against Podunk). Stand firm and it will get better. It will also give you the time needed to find a new f-type toy you'll love.

I have felt your pain. I would suspect that since the vehicle was properly parked and was not running and/or otherwise in use, that this is a "property damage" claim vs an accident claim. There are different standards (at least in Michigan) for compensation including loss of use (car rental even if you weren't insured for that) and I believe the level of depreciation. However, the adjuster is NOT your friend and neither is your insurance company, but when you subrogate (like you have) they actually have to "work" to get your claim processed. Do not be in a hurry, if you can, to settle. The longer you do not settle, the better they will negotiate. Find comps online yourself of truly comparable f-types and show them. Hemmings and Jaguar dealers in high-end communities like Naples, Florida will have the highest prices, not ebay or shitty 2-star used car dealers in Podunk. (Disclaimer: I truly have nothing against Podunk). Stand firm and it will get better. It will also give you the time needed to find a new f-type toy you'll love.

This is not being approached as if it's a property claim, just an auto claim (unfortunately). But, I am definitely not in a hurry. We're doing our best to be treated fairly and with consideration to the facts you have mentioned. We've done a pretty good job so far (I think) of letting the insurance reps know that we are not gonna roll over on this. But, man, these F'ers can be exhausting with their canned responses and advice to accept what we're offered...because it's just how insurance works.

I would pull up some pre owned F-type prices from Jaguar Dealerships and print them out. Especially if they are CPO F-Types. The usually publish the pricing on their websites.

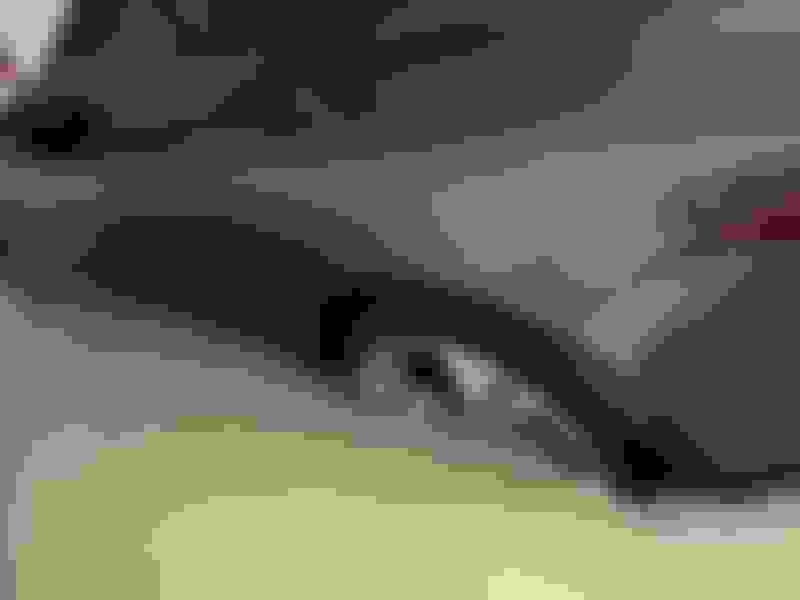

The building hired a contractor to flush out the storm drains. Then, the exact thing happened that they were trying to prevent. Water backed up into the enclosed, under-buiding garage. Oily, silty water was just about up to the windows before anyone working on the project noticed. Then, once the interior of the car was drained, a fire started under the floorboard; which spread into the interior. They put out the fire by dousing the inside of the car with more water.

It's been a week now. I can't say we've recovered emotionally just yet. Waiting on the insurance companies to go through all their red tape. Hopefully, they at least reimburse us for what we paid for the car ...only FOUR MONTHS AGO.

What a kick in the *****. (Pic is after some of the water had been pumped out.)

Sorry to here this, just had my XK totaled, spent $1k on a rental till I found a car. My insurance says I will be reimbursed, but cannot give me a date. Been over a month, hope you have better luck!!

I told my insurance rep right off the bat, that I was going to get an attorney if I was not treated good. Years ago an attorney told me insurance companies will play nice (relatively) if you play the lawyer card up front.

I told my insurance rep right off the bat, that I was going to get an attorney if I was not treated good. Years ago an attorney told me insurance companies will play nice (relatively) if you play the lawyer card up front.

We've just played that card. We'll see what happens.

I would get an attorney to file suit against the contractor for recovery of all costs involved in purchasing, licensing and insuring the vehicle plus emotional damages.

I would include rental costs until case is resolved.

This is clearly a case of total incompetence on their part.

100% this! This should be a legal claim against the contractor - you might want to notify your own insurance but not claim against them at this stage.

The contractor should have their own liability insurance and they would claim against that - but that is their problem not yours.

The building hired a contractor to flush out the storm drains. Then, the exact thing happened that they were trying to prevent. Water backed up into the enclosed, under-buiding garage. Oily, silty water was just about up to the windows before anyone working on the project noticed. Then, once the interior of the car was drained, a fire started under the floorboard; which spread into the interior. They put out the fire by dousing the inside of the car with more water.

It's been a week now. I can't say we've recovered emotionally just yet. Waiting on the insurance companies to go through all their red tape. Hopefully, they at least reimburse us for what we paid for the car ...only FOUR MONTHS AGO.

What a kick in the *****. (Pic is after some of the water had been pumped out.)

The contractors general liability insurance should cover this as it sounds like the work they were performing caused the garage to flood thus creating property damage.

Property damage liability policies have limits too. Might be only $100K. Even if it were $500K it wouldn't take very long to max it out if there's more than a few cars at $100K value. Whomever hired the contractor probably also has a contingent liability. Bankruptcy by the contractor is in the view of all and the OP's auto policy is last on the list. Yeah, a lawyer is the best way to go but after you pay the him/her and still get shafted by whoever's insurance settlement offer its gonna take time and you'll never get even. Best to you!

I’ve been a member of USAA for 32 years. Auto insurance, Credit Cards, vehicle loans (both new and used); they’ve always talked a good game; in March of this year they were put to the test. I didn’t find it necessary to cry lawyer, law suit, etc; a one vehicle accident that I was at fault; USAA took good care of me.

On 8 March I totaled my 2018 Jeep Wrangler Sahara - with less then 12 payments to pay off! After waiting almost 6 weeks for the auto collision center to get their stuff together both the inspectors and appraisers got their heads together I ended up doing quite well. Going back and looking over the purchase documents I financed $25.5K and after deducting the $5.7K I still owed I ended up with a check for $24K! I used that as a down payment on my “F” Type convertible and currently only owe just north of $17K.

05-25-2023, 05:44 PM

05-25-2023, 05:44 PM

(Pic is after some of the water had been pumped out.)

(Pic is after some of the water had been pumped out.)