When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

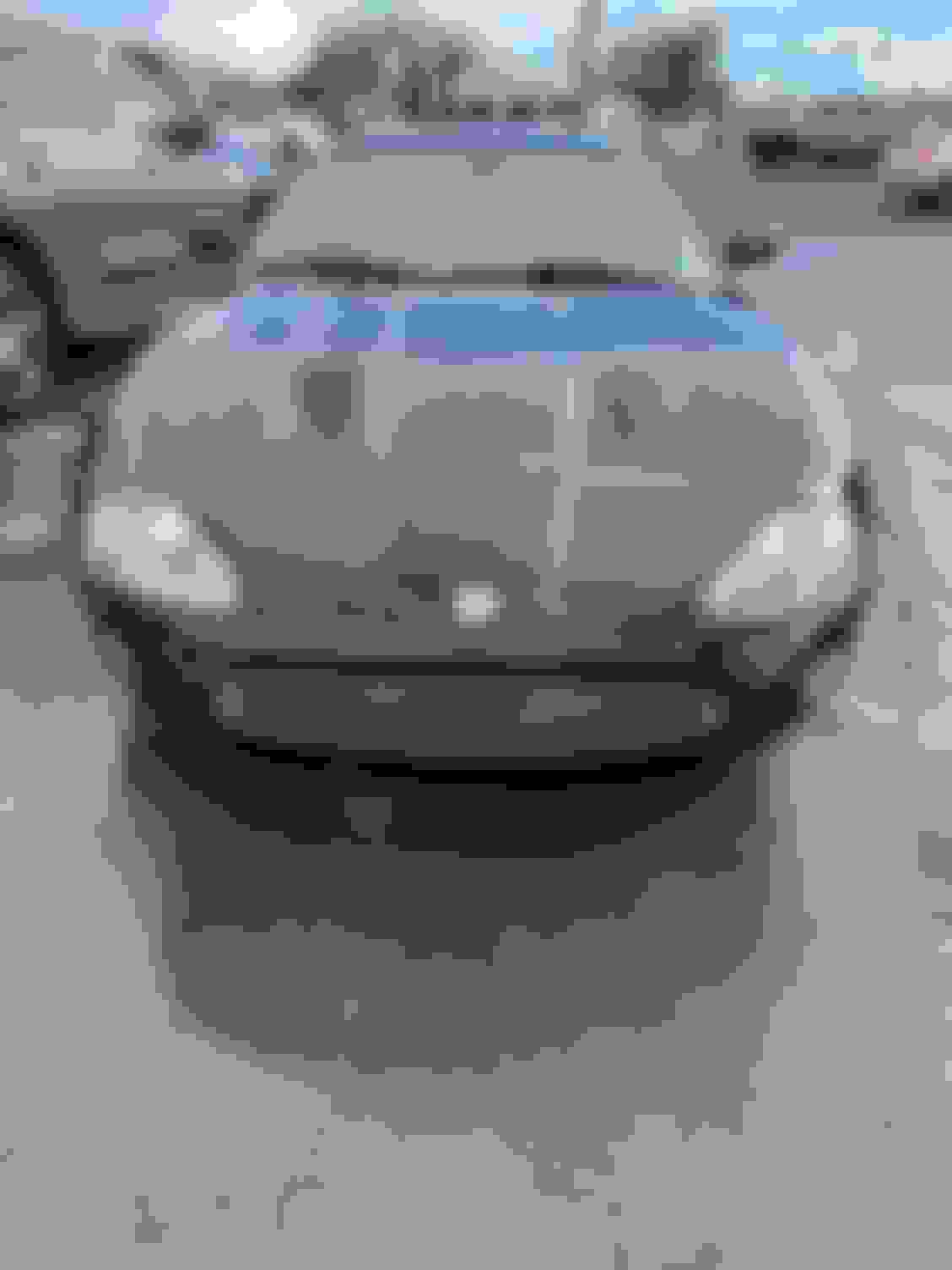

A drunk crossed Center Line and hit my 2005 Carbon Fiber Edition. His Insurance Co. has admitted he was in the wrong. Kind of hard to deny when there are 2 different Videos that show what happened. His Insurance Co is talking about totaling my Car. I would of course like it to be fixed. Car starts and seem to run okay. I had it towed because the Fender was rubbing against the tire. Car had no issues before the wreck. I know it's hard to tell from just Pictures but does anyone have a general idea on what the repairs would be. Hood, Bumper, Fender and Headlight. It was a pretty low speed collision so I wouldn't think there is any frame damage. If I can't get them to repair any idea what a reasonable price to would be accept would be? Car has about 110,000 miles.

Used parts won't be too bad at least they aren't in the UK. Front bumper is around �200 or so, bonnet around �500 and the front wing around �100 depending on the colour and condition. Then it's just labour and stuff. The front headlight might not be cheap and you have all the parts inside that look smashed up. I think you could probably do it all for around �2k? But someone with more experience will have a better idea with this car.

Sorry to hear that. It does not take much damage these days to total an XK8 / XKR. Hope you are able to squeeze enough money out of the insurance company to repair the car if you so choose. Keep us posted....

After going getting hit a number of times by inattentive drivers, here are some lessons I've learned (as someone who is not a lawyer):

0. You are an amateur going up against pros in this game. If your Insurance Company (IC) isn't liable for the costs, then they are going to be your best friend. Otherwise, you have to treat your IC as an adversary.

1. If possible, keep your car in your possession.

Make their insurance adjuster come to you at your convenience to inspect the damage.

2. Demand that their IC gets you a comparable rental car with full insurance coverage.

The mounting price of this will pressure their IC to not drag their feet on the settlement process. But also see #7 below

3. My buy-back price of a totaled car was ~10% of the payoff amount, but you will now have to title your vehicle as a salvage vehicle. My impression is that most ICs won't compensate you for full value if the vehicle gets totaled again. But some do.

4. Don't expect a fair value assessment from their IC.

The IC for the kid who totaled my old audi convertible offered me a very low ball amount. I refused it and I had my IC (who wasn't having to pay for the wreck) to send out their adjuster, who correctly assessed it at 2x the first estimate. I took my IC's settlement and let the two ICs fight it out.

5. Don't expect a fair value assessment from their IC.

They will look for comparable vehicles in the region and pick the worse ones. Demand to see their list of comparables. I researched and contacted some of their comparables and discovered they were using parts cars and non-runners off craigslist to generate their numbers. Come up with your own list of comparable values.

6. Don't expect a fair value assessment from their IC.

The adjuster will generate a comparable number, then come out, inspect your vehicle. If the adjuster is from the IC that is paying, the adjuster will lower the assessed value substantially based on any flaws they can find on your vehicle, such as rock-chips, worn seat/carpet, oil on the ground, dents etc. Don't allow this as it double penalizes you because your vehicle's current As-Is condition is already reflected in the average price of the comparables, which are also "As-Is" and not perfect. Next time I get hit, I'm immediately getting my vehicle professionally detailed by a mobile service before any adjuster sees it.

7. Don't expect a fair value assessment from their IC.

Once their IC offers you their low-ball settlement offer, that starts the clock for you to lose the rental car in a day or so, even if the offer is ridiculously unrealistically low. No matter how nice they seem, the other persons IC and their inspectors have your worst interests at heart.

8. You will take an unfair loss on this.

You won't be compensated for your lost time or the fact that you are now being forced to unwillingly sell your vehicle that you had no intention of selling (if it is totaled out). Both of these have a real value that you won't be able to recover from the other driver's IC.

9. If your vehicle is not totaled and is rebuilt, research getting compensated for "diminished value" due to the accident and rebuild now showing up on its carfax history.

The bottom line here is that there is little reason for you to be nice or polite or reasonable about any of this situation. That drunk driver made an intentional choice that put your life at risk and now they are costing you your precious time and focus dealing with the aftermath, with no compensation to you other than repairing/totalling your car.

After going getting hit a number of times by inattentive drivers, here are some lessons I've learned (as someone who is not a lawyer):

0. You are an amateur going up against pros in this game. If your Insurance Company (IC) isn't liable for the costs, then they are going to be your best friend. Otherwise, you have to treat your IC as an adversary.

1. If possible, keep your car in your possession.

Make their insurance adjuster come to you at your convenience to inspect the damage.

2. Demand that their IC gets you a comparable rental car with full insurance coverage.

The mounting price of this will pressure their IC to not drag their feet on the settlement process. But also see #7 below

3. My buy-back price of a totaled car was ~10% of the payoff amount, but you will now have to title your vehicle as a salvage vehicle. My impression is that most ICs won't compensate you for full value if the vehicle gets totaled again. But some do.

4. Don't expect a fair value assessment from their IC.

The IC for the kid who totaled my old audi convertible offered me a very low ball amount. I refused it and I had my IC (who wasn't having to pay for the wreck) to send out their adjuster, who correctly assessed it at 2x the first estimate. I took my IC's settlement and let the two ICs fight it out.

5. Don't expect a fair value assessment from their IC.

They will look for comparable vehicles in the region and pick the worse ones. Demand to see their list of comparables. I researched and contacted some of their comparables and discovered they were using parts cars and non-runners off craigslist to generate their numbers. Come up with your own list of comparable values.

6. Don't expect a fair value assessment from their IC.

The adjuster will generate a comparable number, then come out, inspect your vehicle. If the adjuster is from the IC that is paying, the adjuster will lower the assessed value substantially based on any flaws they can find on your vehicle, such as rock-chips, worn seat/carpet, oil on the ground, dents etc. Don't allow this as it double penalizes you because your vehicle's current As-Is condition is already reflected in the average price of the comparables, which are also "As-Is" and not perfect. Next time I get hit, I'm immediately getting my vehicle professionally detailed by a mobile service before any adjuster sees it.

7. Don't expect a fair value assessment from their IC.

Once their IC offers you their low-ball settlement offer, that starts the clock for you to lose the rental car in a day or so, even if the offer is ridiculously unrealistically low. No matter how nice they seem, the other persons IC and their inspectors have your worst interests at heart.

8. You will take an unfair loss on this.

You won't be compensated for your lost time or the fact that you are now being forced to unwillingly sell your vehicle that you had no intention of selling (if it is totaled out). Both of these have a real value that you won't be able to recover from the other driver's IC.

9. If your vehicle is not totaled and is rebuilt, research getting compensated for "diminished value" due to the accident and rebuild now showing up on its carfax history.

The bottom line here is that there is little reason for you to be nice or polite or reasonable about any of this situation. That drunk driver made an intentional choice that put your life at risk and now they are costing you your precious time and focus dealing with the aftermath, with no compensation to you other than repairing/totalling your car.

This is fantastic advice that I sure hope to never have to heed!

If you don't mind, what's the coverage in your insurance policy? I didn't opt for Haggerty's Cherished Salvage, but maybe I should?

Thanks!

I have three X100s insured with Hagerty. I got declared value and the Cherished Salvage Coverage 'just-in-case'.

A customer of mine got a 1998 XK8 in nice condition insured with Hagerty for a declared value of $15000.00 and Cherished Salvage for 300 or 400 hundred dollars a year.

No arguing when you have declared value.

Picked up Rental Car this morning. Don't plan to drive it but they are paying so I got it. Latest word is they are towing my Car to Baton Rouge, La. (I live in Lafayette, La.) to a Progressive Assessment Yard and will decide if they are going to total it or fix it.

Used parts won't be too bad at least they aren't in the UK. Front bumper is around �200 or so, bonnet around �500 and the front wing around �100 depending on the colour and condition. Then it's just labour and stuff. The front headlight might not be cheap and you have all the parts inside that look smashed up. I think you could probably do it all for around �2k? But someone with more experience will have a better idea with this car.

I think you're looking at $10k plus, easy. For repair quote new part prices will be considered or labor for body/paint work which with today's hourly rates will add up quickly. It is salvageable for sure, but not surprised insurance just wants to total it. What a waste, but consider that it could have been much worse...

If you want/can work on it yourself then it still will be a challenge to find used parts.

Hope things work out for you.

The long reply above is all good advice. I had a similar situation last winter. From end damage from low speed impact

Body shop prelim estimate was $5800 to repair. The insurance company at first did not recognize the car a unique in any way. Insurance co estimated car value at about 9000 but expected hidden damage including impact bar and possible frame tweak to move repair estimate to a higher level. They wanted to total the car and offered me about $8 for it. I tried to deny their total and withdraw my claim but once the claim was filed they took control. I asked body shop to change their prelim estimate to a final to lock in the max they would charge and they did at ~$8k. Then I found recent auction results for Victory Edition carbon fiber coupes sales on line which ranged from $15k - $20k and submitted those to insurance co. Based on that they sent their estimator out to inspect and estimate repair. He came up with similar numbers to mine and the insurance co declared my car value at $15,500 and transferred claim out of the total loss area back to repair claim area. They sent me a check for $8200 for repair. Body shop did the work and because the headlight only had a small scratch did not replace that. Final bill from body shop $6,900. So I had body shop do some more work and a ceramic coat.

So don�t give up! If you can get support for value and a good body shop to quote repair cost firmly, you may be able to keep it. Plus I have an agreed upon market value documented at upwards of $15,500.

Really timely conversation about Hagerty. With my insurance policy coming due and my rates going up (like everyone’s ) I decided to shop collectors insurance companies for my Jag and Hagerty was best value. My other coverage was for liability only now after switching I have full coverage along with towing and road service for the same price. I’ve had collectors coverage in the past with other cars and honestly I don’t know why I didn’t do it sooner with my Jag.

My car shows an accident on Carfax. When I contacted the old owner he sent me a picture of the damage.

Yes, this was the extent of the accident. Kinda blows it’s on my title

Research diminished value claims. I had a brand new (less than 30 days old) Jeep 4xe that was hit by someone who ran a red light. I repaired it (we both had the same insurance), but they refused the diminished value claim. I am a lawyer and sued in limited action court for $7,500. I settled for about $5,000 after I told the lawyers they hired that I could do my legal work for free and this would cost them way more than what I wanted to address the reduced value of the vehicle. Do not give up on this aspect of your claim even if they pay for the right repairs.

I got my first offer from the Insurance Co. It was pretty close to what I expected. I made a counteroffer. They said they would get back to me today. They said they only found one deficiency on my car. Hinge Cover was missing on Drivers Seat. I told their Rep that I had that piece and could send picture if necessary. There reason for low offer was mileage on car (130,000). Since this has happened, I have been looking at Valuation Sites. NADA seems to be very low compared to KBB and others that I have seen.

You need to do a THUROUGH search for like cars & condition & what they have sold for. Look on sites such as Bring a Trailer & Haggerty. Document the value of carbon fiber edition models - don't let them lowball you. If they want to repair it, take it to a shop of YOUR CHOOSING & make sure they use OEM parts - also get an estimate for Diminished Value. They are responsible to MAKE YOU WHOLE, & that includes ALL expenses occurred. I used to have the site Screwed By Insurance .com (check the wayback machine), & I can tell you the insurance CARTEL will screw you over if you let them.

I just got an email from Hagerty that the value of base model XKR 2000MY in GOOD condition is up from $16500.00 to $17800.00 for OCT 2024.

$29300.00 for Excellent.

Insurnace Co. made 2nd offer which was about 45% better than the 1st. It was close to the minimum that I had decided to accept but not what I though the car was worth. While waiting for my check I started shopping to replace my XK8. I found a couple I thought might be interesting to look at. They were at used car dealerships from 400 to 600 miles away so hard to go test drive. Did review search on both. Reviews for both dealerships were bad averaging 1 to 2 stars on 10+ reviews. I did find one that was supposed to be a private sale about 200 miles away on Auto Trader. I sent a message to owner but never got a response. I will continue to search. Looking for 4.2 Convertible. I'm not too concerned with mileage. After owning 2 of these I think the more they are driven the better they run.

09-27-2024 | 06:04 AM

09-27-2024 | 06:04 AM